If you’re self-employed and work with international clients, maintain foreign business accounts, or operate as a digital nomad, you face critical tax compliance requirements beyond typical self-employment tax obligations.

One requirement many freelancers and micro-business owners overlook is the Foreign Bank and Financial Accounts Report (FBAR) – and the penalties for non-compliance can be financially devastating. If you’ve already missed FBAR filings, the IRS streamlined domestic offshore procedures may provide a pathway back to compliance.

What is FBAR, and why do self-employed individuals need to care

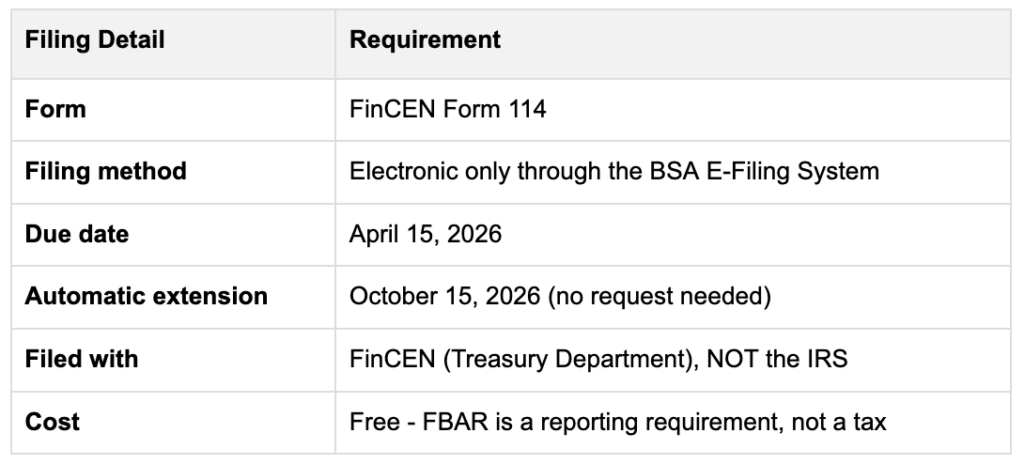

The FBAR (FinCEN Form 114) is a reporting requirement mandated by the Bank Secrecy Act that requires US persons to report foreign financial accounts to the Treasury Department’s Financial Crimes Enforcement Network (FinCEN). Unlike income tax forms filed with the IRS, FBARs are filed separately through the BSA E-Filing System.

For self-employed professionals, this becomes relevant when you:

- Accept payments through foreign payment processors like Wise, PayPal international accounts, or Payoneer

- Open foreign business bank accounts for better currency management

- Maintain checking or savings accounts abroad while working as a digital nomad

- Have signature authority over a foreign client’s or partner’s business accounts

FBAR filing thresholds

You must file an FBAR if the aggregate maximum value of all your foreign financial accounts exceeded $10,000 at any time during the calendar year – even for a single day. The threshold is cumulative across all foreign accounts combined, not per account.

Example: If you have three foreign accounts with balances of $4,000, $3,500, and $3,000 that collectively exceed $10,000 at any point during the year, you must file.

Which foreign accounts require reporting

FBAR requirements extend beyond traditional bank accounts to include:

- Business accounts: Foreign checking, savings, and business operating accounts

- Investment accounts: Foreign brokerage accounts, mutual funds, and pooled investment vehicles

- Payment processor accounts: Foreign-based accounts with Wise, Revolut, or similar platforms holding balances

- Retirement accounts: Certain foreign employer pension plans or retirement savings

- Accounts with signature authority: Foreign business accounts where you can control funds even if you don’t own the account

For self-employed individuals running foreign businesses or serving as officers in foreign entities, you must also report accounts where you have signature authority – a requirement that catches many freelance consultants by surprise.

Self-employment tax and foreign income: The double burden

Self-employed expats face a unique challenge: while the Foreign Earned Income Exclusion (FEIE) can reduce your regular income tax, it does not reduce your self-employment tax. You must pay self-employment tax (Social Security and Medicare tax) on all net earnings from self-employment if your net earnings are $400 or more, whether you’re living in the United States or abroad.

Self-employed individuals essentially pay both the employer and employee portions of Social Security and Medicare taxes – 15.3% total – on their net business profit.

Example: A freelance consultant living in Spain earns $95,000 with $27,000 in business deductions, resulting in $68,000 net profit. Even if she excludes $68,000 from income tax using the FEIE, she must still pay the full 15.3% self-employment tax on the $68,000.

This creates a compliance burden where self-employed expats must report foreign income for self-employment tax purposes (Schedule SE), file FBAR if foreign account balances exceed $10,000, and potentially file FATCA Form 8938 if they meet higher reporting thresholds.

FBAR filing deadlines and process for 2026

FBAR is filed separately from your federal tax return. You must file even if your foreign accounts generated no income or you owe no US taxes.

Penalties for non-compliance

FBAR penalties are among the most severe in tax law. For 2026:

- Non-willful violations: Up to $16,536 per violation

- Willful violations: Greater of $165,353 or 50% of account balance per violation

- Criminal penalties: Up to $500,000 in fines and 10 years imprisonment for willful failures

For self-employed individuals who unknowingly failed to file FBARs while managing foreign business accounts, these penalties can devastate a small business financially.

Common FBAR mistakes self-employed individuals make

- Assuming payment processor accounts don’t count: Many freelancers don’t realize foreign-based Wise or Payoneer accounts qualify as foreign financial accounts requiring FBAR reporting.

- Thinking per-account thresholds apply: The $10,000 threshold is aggregate across all accounts, not per account.

- Confusing FBAR with tax forms: FBAR is filed with FinCEN through a separate system, not with the IRS alongside your tax return.

- Overlooking signature authority: Having control over a foreign client’s account creates filing obligations even if you don’t own the account.

- Missing totalization agreement exemptions: Some self-employed individuals may qualify for exemptions from dual social security taxation under international agreements, but these require proper documentation.

International tax compliance checklist for self-employed

Self-employed individuals working internationally face multiple compliance layers:

- Quarterly estimated tax payments, including self-employment tax on foreign earnings

- FBAR filing when foreign account balances exceed $10,000

- Form 8938 (FATCA) for higher-value foreign assets

- Foreign income reporting on Form 104,0 even when using exclusions or credits

- Form 1099 reporting for payments to foreign contractors

- Understanding totalization agreements for potential social security exemptions

Tracking reportable income and maintaining proper documentation becomes essential for federal tax compliance when working with international clients or receiving payments through international channels.

What to do if you’ve missed FBAR filings

If you’ve failed to file FBARs in previous years, don’t ignore the problem. The IRS offers compliance pathways for those with unreported foreign accounts, including the IRS streamlined domestic offshore procedures for taxpayers whose failures were non-willful.

These programs allow eligible taxpayers to come into compliance while potentially reducing or eliminating penalties – critical for self-employed individuals who may have innocently overlooked reporting requirements while building their international business.

The streamlined procedures are specifically designed for taxpayers who can certify their non-compliance was non-willful, offering a pathway back to compliance without the devastating penalties typically associated with FBAR violations.

Protecting your self-employed business

International tax compliance for freelancers requires proactive management:

- Track balances monthly: Document maximum balances for all foreign accounts throughout the year

- Understand SE tax obligations: The Foreign Earned Income Exclusion does not eliminate self-employment tax

- Mark your calendar: April 15 deadline with automatic extension to October 15

- File separately: FBAR goes to FinCEN, not the IRS

- Consult professionals: Expat tax specialists understand the unique challenges self-employed expats face

- Stay current: Tax laws and reporting thresholds change regularly

As a self-employed professional working internationally, federal tax compliance extends far beyond calculating income tax on self-employed earnings. Missing FBAR requirements can result in penalties that eclipse your actual tax liability, making awareness and compliance essential for protecting your business and financial future.